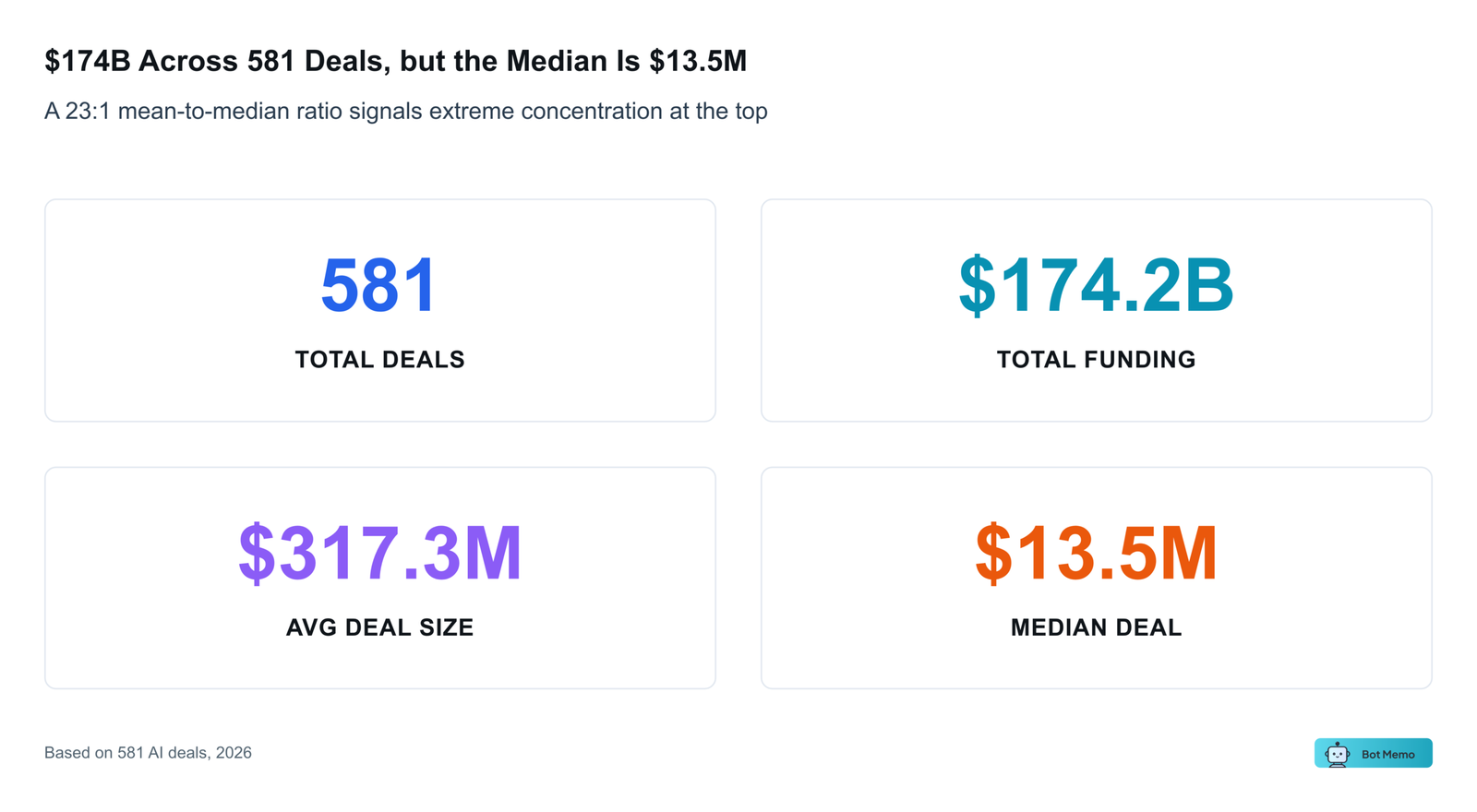

March 2026 AI funding totaled $174.2 billion across 581 deals. That number demands a disclaimer before anything else: OpenAI closed a $122 billion round on March 31, accounting for 70% of the month’s total. The fundraise began on February 27 with $110 billion in commitments and added $12 billion more by close. We attribute it to March because that’s when it closed. Anthropic’s $30 billion Series G closed on February 12 and is not included in these figures.

Strip OpenAI out and March drops to $52 billion across 580 deals. That’s still a massive month by any historical standard, but it tells a very different story about the market.

Bot Memo tracked every publicly announced round to build this analysis. Here’s what the data shows when you look past the headline.

On this page

- The Three-Company Problem

- Where the Money Went: Infrastructure Absorbs 82%

- Defense AI's $7.75 Billion Month

- Geographic Concentration: San Francisco and Everyone Else

- Funding Stages: Seed Leads by Count, "Other" Dominates by Dollars

- What Founders and Investors Are Building

- The Most Active Investors

- What March 2026 Actually Tells Us

The Three-Company Problem

Three checks totaling $110 billion defined March. Amazon put $50 billion into OpenAI. Nvidia and SoftBank each committed $30 billion. Andreessen Horowitz and D.E. Shaw Ventures participated as well, and for the first time, OpenAI opened participation to retail investors through bank channels, raising $3 billion from individuals.

The resulting $122 billion round valued OpenAI at $852 billion post-money. Revenue had crossed $2 billion a month.

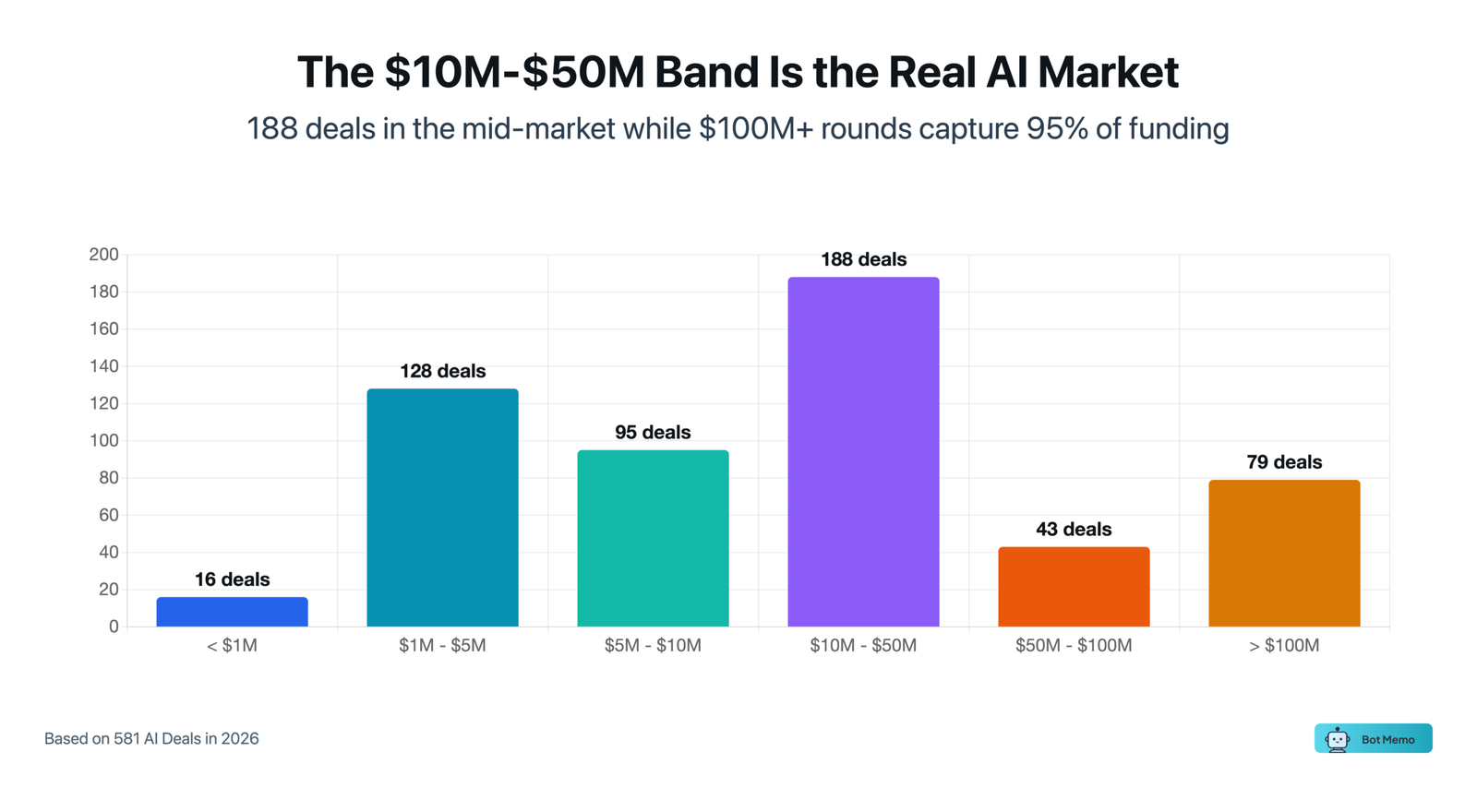

To understand the distortion: the mean deal size for March was $317 million. The median was $13.5 million. That 23:1 ratio is the single clearest indicator of how concentrated the capital stack has become. The typical AI startup raised a mid-eight-figure round. The headline number is an infrastructure financing story.

CoreWeave’s $8.5B Is Debt, Not Equity

One clarification that matters: CoreWeave’s $8.5 billion is a delayed-draw term loan facility secured by GPU hardware and a $19 billion+ contract with Meta. It achieved the first investment-grade rating (A3/A-low) for GPU-backed infrastructure financing. CoreWeave trades publicly as CRWV. This isn’t a startup fundraise. It’s a signal that AI infrastructure has matured enough for bond-market-style financing.

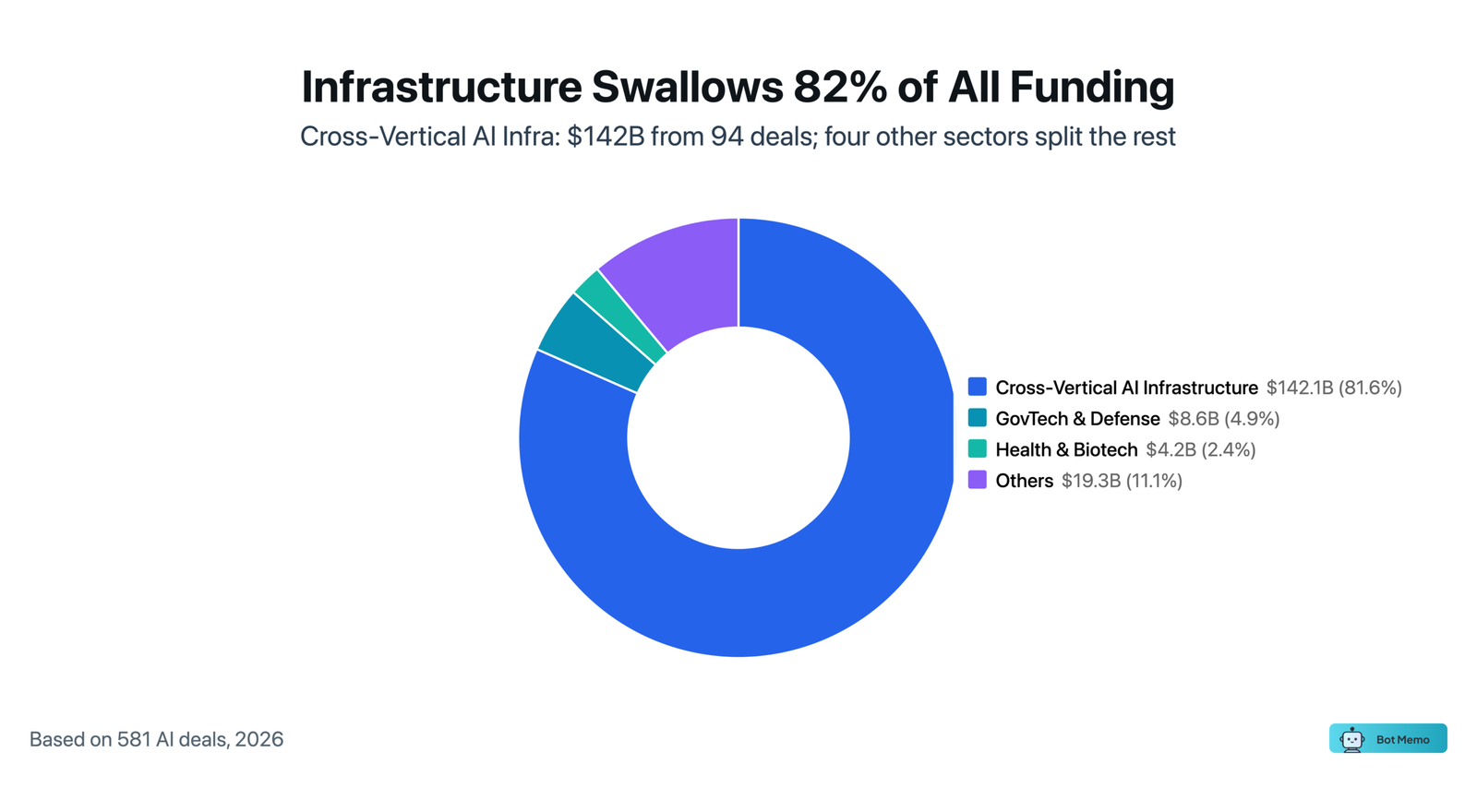

Where the Money Went: Infrastructure Absorbs 82%

Cross-Vertical AI Infrastructure captured $142.1 billion across 94 deals, or 82% of total March funding. Even excluding OpenAI, infrastructure still dominates because of CoreWeave ($8.5B), plus substantial rounds in cloud computing and GPU-adjacent companies.

The application layer told a different story by deal count. Health & Biotech led with 91 deals ($4.2B), followed by Enterprise Software at 82 deals ($2.0B) and FinTech at 71 deals ($1.8B). The application economy is active, funded, and building, but the dollar volumes are two orders of magnitude smaller than infrastructure.

| Sector | Funding | Deals | % of Total |

|---|---|---|---|

| Cross-Vertical AI Infrastructure | $142.1B | 94 | 82% |

| GovTech & Defense | $8.6B | 18 | 5% |

| Health & Biotech | $4.2B | 91 | 2% |

| Transportation & Mobility | $3.3B | 36 | 2% |

| Manufacturing & Industrials | $3.2B | 26 | 2% |

| Energy & Sustainability | $2.6B | 23 | 2% |

| Enterprise Software | $2.0B | 82 | 1% |

| Cybersecurity | $1.8B | 43 | 1% |

| FinTech | $1.8B | 71 | 1% |

Source: Bot Memo analysis of 581 AI deals (March 2026)

Defense AI’s $7.75 Billion Month

Three defense AI companies raised a combined $7.75 billion in March, making GovTech & Defense the second-largest sector by funding volume:

Anduril Industries closed $4 billion at a $60 billion valuation, led by Thrive Capital and a16z. The company is building a 5-million-square-foot autonomous weapons manufacturing facility in Ohio. The round is about production capacity, not R&D.

Shield AI raised $2 billion in a Series G at $12.7 billion valuation, tied directly to a U.S. Air Force contract. The 140% valuation jump from its previous round reflects government procurement, not commercial traction.

Saronic Technologies closed $1.75 billion at $9.25 billion for autonomous warships. A Series D of that size for a naval autonomy company was unthinkable two years ago.

The common thread: these are not software companies selling licenses. They are manufacturers building physical systems at scale, and the capital requirements reflect it.

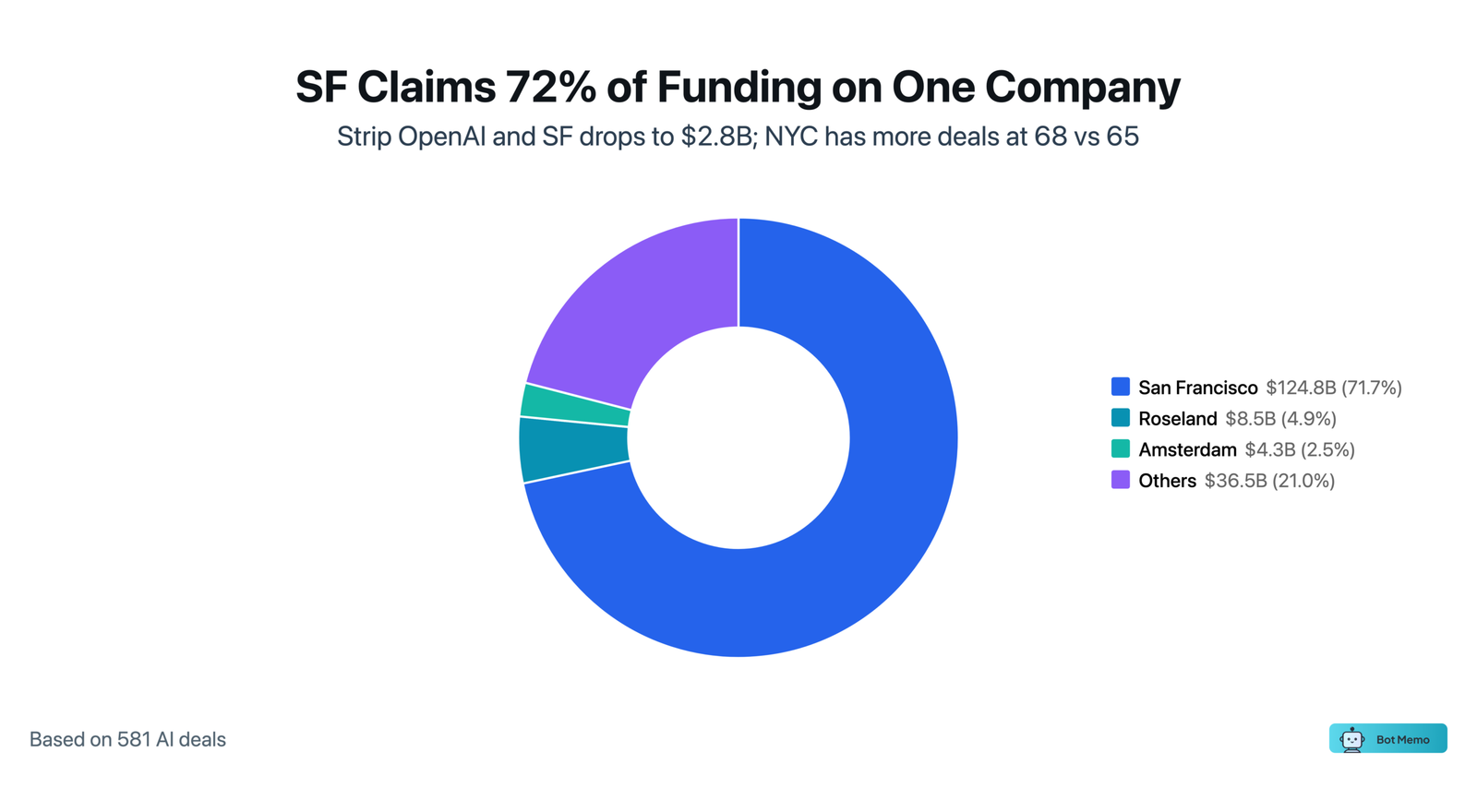

Geographic Concentration: San Francisco and Everyone Else

San Francisco accounted for 71.7% of total funding ($124.8B) across 65 deals, almost entirely driven by OpenAI’s headquarters being in the city. Remove that single round and SF’s share drops below 5%.

The more interesting geographic picture emerges outside the mega-round distortion:

| City | Funding | Deals | Mean Deal |

|---|---|---|---|

| San Francisco | $124.8B | 65 | $1.92B |

| Roseland, NJ | $8.5B | 1 | $8.5B |

| Amsterdam | $4.3B | 4 | $1.08B |

| Costa Mesa | $4.0B | 1 | $4.0B |

| Paris | $3.2B | 13 | $245M |

| New York City | $3.2B | 68 | $47M |

| London | $2.9B | 34 | $85M |

| San Diego | $2.1B | 5 | $416M |

| Austin | $1.9B | 10 | $191M |

| Beijing | $1.8B | 7 | $260M |

Source: Bot Memo analysis of 581 AI deals (March 2026). Multi-city companies attributed to each HQ location.

New York City led on deal volume (68 deals) despite ranking sixth in funding, pointing to an active early-stage and mid-market ecosystem. London’s 34 deals at a $85 million average and Paris’s 13 deals at $245 million average reflect Europe’s different capital structures. Bangalore’s 20 deals at $37 million average confirm India’s growing AI startup scene at smaller check sizes. For city-level breakdowns, see our reports on AI startups in San Francisco, New York, and London.

Roseland (CoreWeave) and Costa Mesa (Anduril) appear because single mega-rounds can place any city on the map.

Funding Stages: Seed Leads by Count, “Other” Dominates by Dollars

The stage distribution reveals a familiar pattern: early-stage activity is broad, late-stage capital is concentrated.

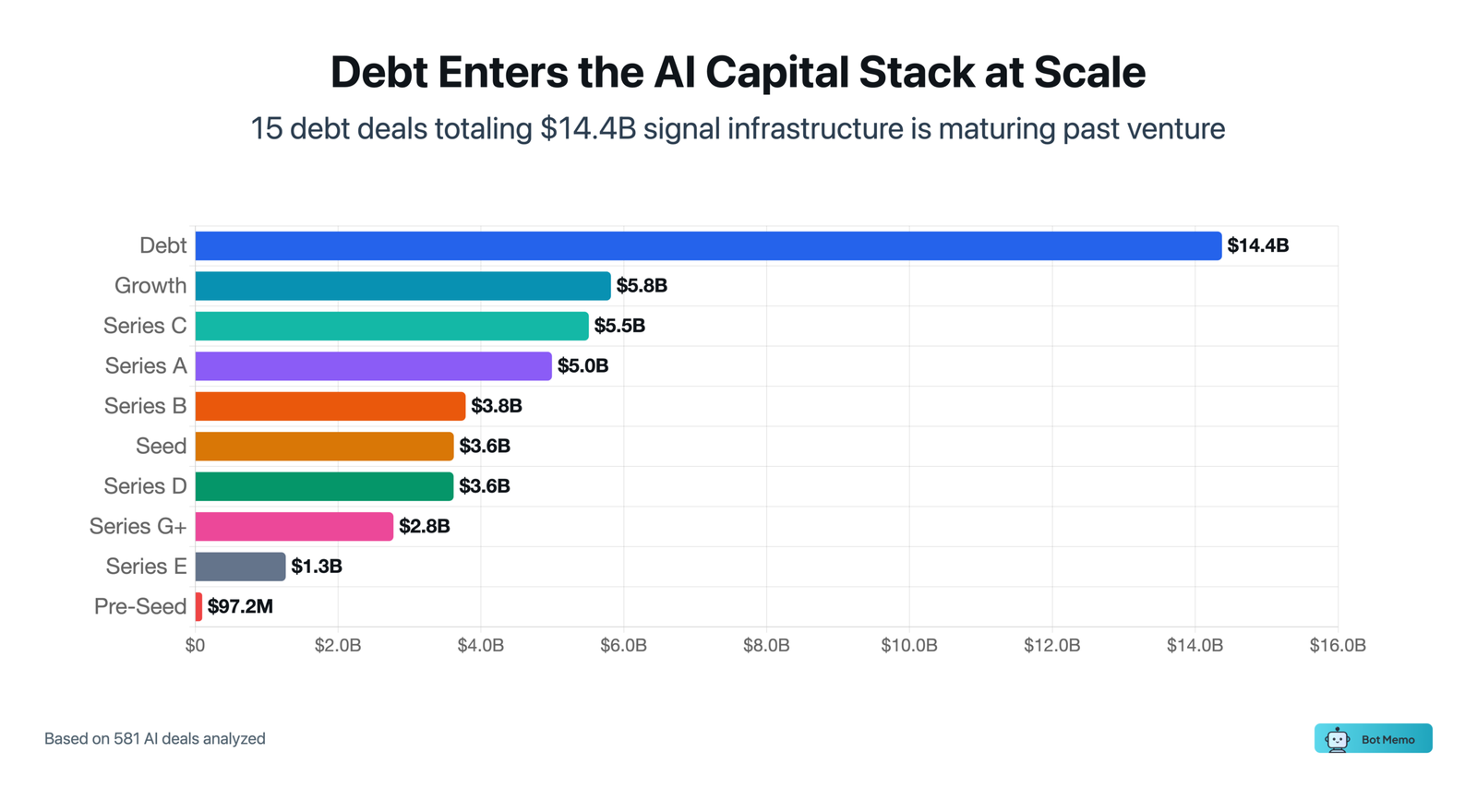

| Stage | Funding | Deals |

|---|---|---|

| Seed | $3.6B | 190 |

| Series A | $5.0B | 120 |

| Series B | $3.8B | 62 |

| Series C | $5.5B | 35 |

| Debt | $14.4B | 15 |

| Growth | $5.8B | 20 |

| Other | $128.4B | 78 |

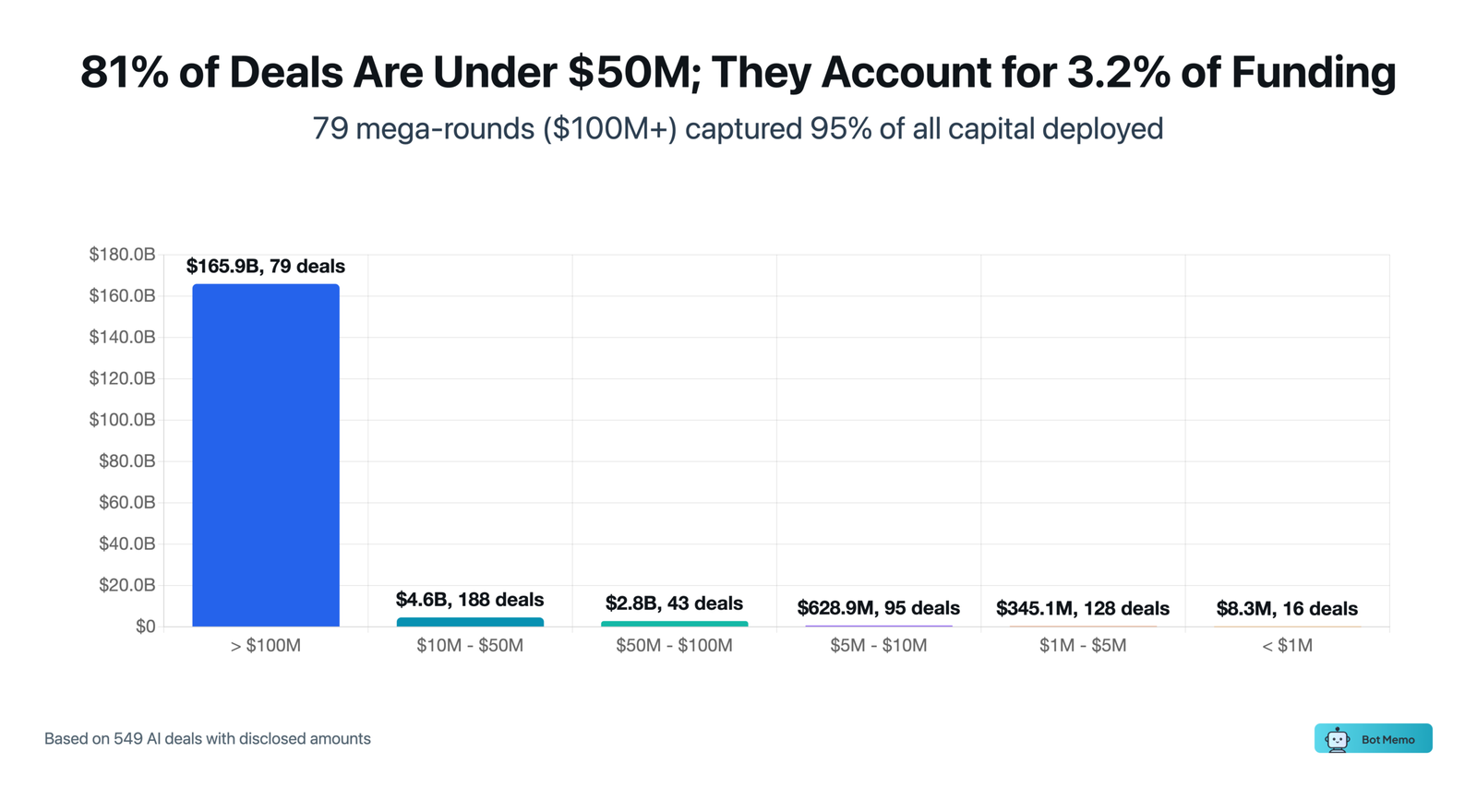

Seed rounds accounted for 190 of 581 deals (33%), confirming that new company formation in AI isn’t slowing down. Series A added another 120 deals. Together, Seed and Series A made up 53% of all March deals but just 5% of total funding. That’s the 23:1 mean-to-median ratio showing up in the stage data: the deal count lives at the bottom, the dollars live at the top.

The “Other” category ($128.4B across 78 deals) includes OpenAI and other mega-rounds that don’t fit standard series labels. Debt financing ($14.4B across 15 deals) is worth watching closely. CoreWeave’s $8.5B term loan is the largest single item here, but 14 other companies also tapped credit markets in a single month. That’s a structural shift: AI infrastructure companies are borrowing against contracts and hardware rather than diluting equity. It won’t show up in a VC funding headline, but it’s changing how the capital stack works.

Pre-Seed activity (42 deals, $97M total) suggests the startup pipeline continues to fill.

What Founders and Investors Are Building

AI Agents dominated March 2026 AI funding by application type, appearing in 221 deals totaling $14.4 billion. That’s 38% of all deals in the month. Data Management (52 deals, $6.4B) and Generative AI (51 deals, $124.8B) followed. Compliance Automation hit 48 deals ($1.2B), which tells you something about where enterprises are spending first: governance and process control, not moonshots.

Robotics drew $5.8 billion across 44 deals. Combined with defense tech and manufacturing, the physical-AI thesis attracted more capital in March 2026 than at any point in the past two years. If you’re a founder building in pure software, the capital competition from hardware-AI companies is real and growing.

Reasoning Models appeared in 24 deals totaling $2.9 billion, a tag that barely existed six months ago.

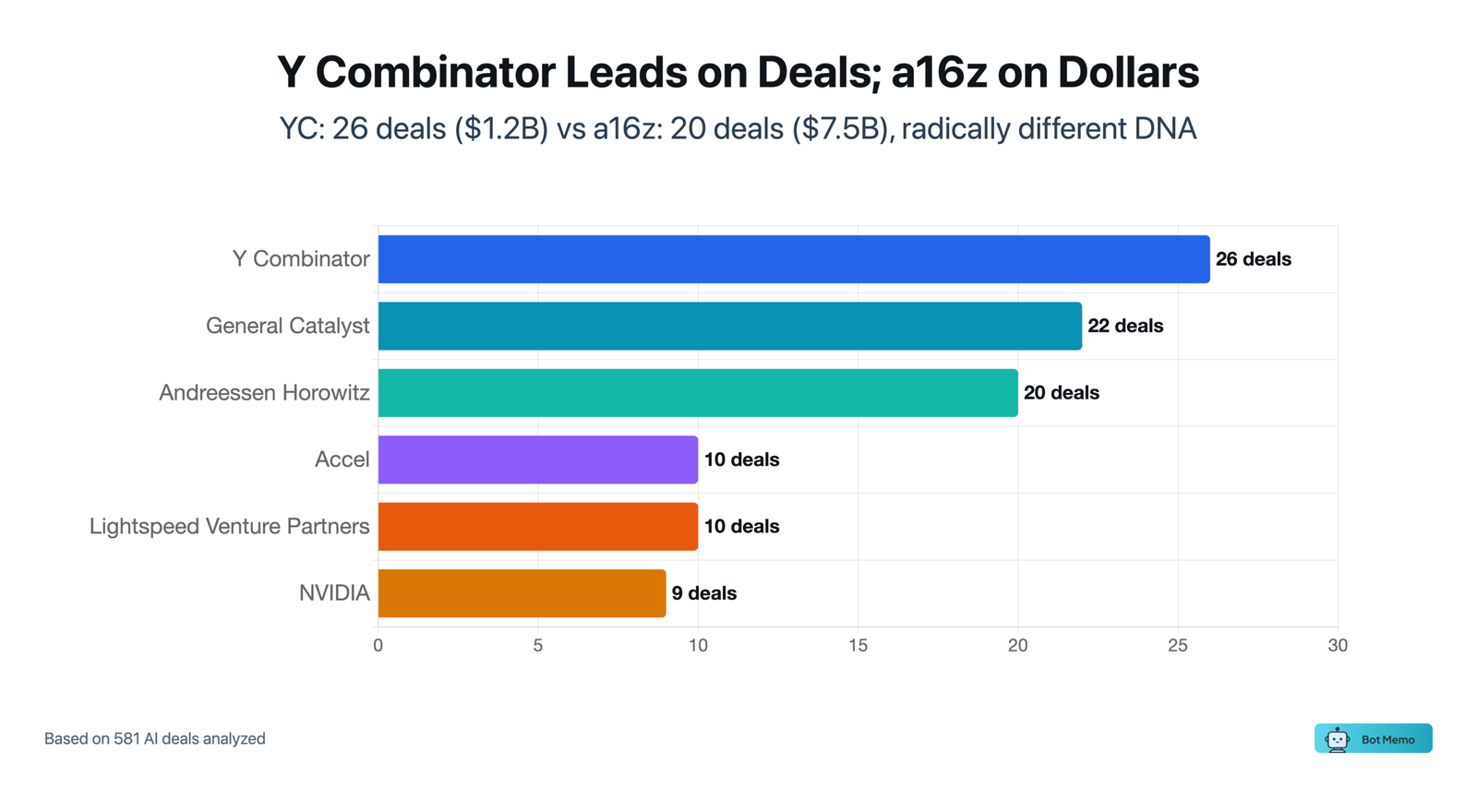

The Most Active Investors

Y Combinator participated in 26 deals (the most of any investor by deal count), followed by General Catalyst (22), Andreessen Horowitz (20), and Accel (10). The concentration of a16z in both deal count and dollar volume ($7.5B across 20 deals) reflects the firm’s outsized position in AI infrastructure.

| Investor | Deals | Participated In |

|---|---|---|

| Y Combinator | 26 | $1.2B |

| General Catalyst | 22 | $1.0B |

| Andreessen Horowitz | 20 | $7.5B |

| Accel | 10 | $1.2B |

| Lightspeed Venture Partners | 10 | $1.1B |

| NVIDIA | 9 | $130.9B |

| Bessemer Venture Partners | 9 | $2.4B |

| 8VC | 9 | $2.2B |

| Sequoia Capital | 8 | $626M |

| Menlo Ventures | 8 | $916M |

Note: Dollar figures represent total funding in deals where the investor participated, not the investor’s individual check size.

NVIDIA’s $130.9 billion in participated deals is driven almost entirely by its $30 billion commitment to OpenAI plus ancillary investments. Sequoia Capital’s 8 deals at $626 million in total participated funding shows a more diversified, smaller-check approach.

What March 2026 Actually Tells Us

The headline ($174.2 billion) describes a market that almost nobody operates in. Three checks wrote $110 billion of it. One company captured 70% of the total.

The market most founders and investors actually occupy, the one below $500 million per round, deployed roughly $25 billion across 560+ deals. Seed and Series A activity is strong. Health, cybersecurity, and enterprise software are drawing steady capital. Defense tech has become a real asset class. And 38% of all deals involved AI agents, making it the single most crowded application category.

The application layer is where the deal count is, and deal count is what eventually determines which sectors produce the next generation of breakout companies. For a deeper look at how March 2026 AI funding fits into the broader year, see our AI Funding 2025 Year in Review for historical comparison.

Note: This analysis is based on Bot Memo’s tracking of 581 publicly announced AI deals in March 2026.

OpenAI’s $122B round began fundraising in February and announced it on their official website on March 31, 2026. We attribute it to March (close date). Anthropic’s $30B Series G closed February 12 and is excluded from March data.

About the author

Editorial Staff

The Editorial Staff at Bot Memo is a team of writers, analysts, and AI agents dedicated to mapping the global AI startup ecosystem. Led by Chintan Zalani, the team tracks thousands of funding rounds, classifies companies across verticals, and distills it all into actionable intelligence for investors and founders.