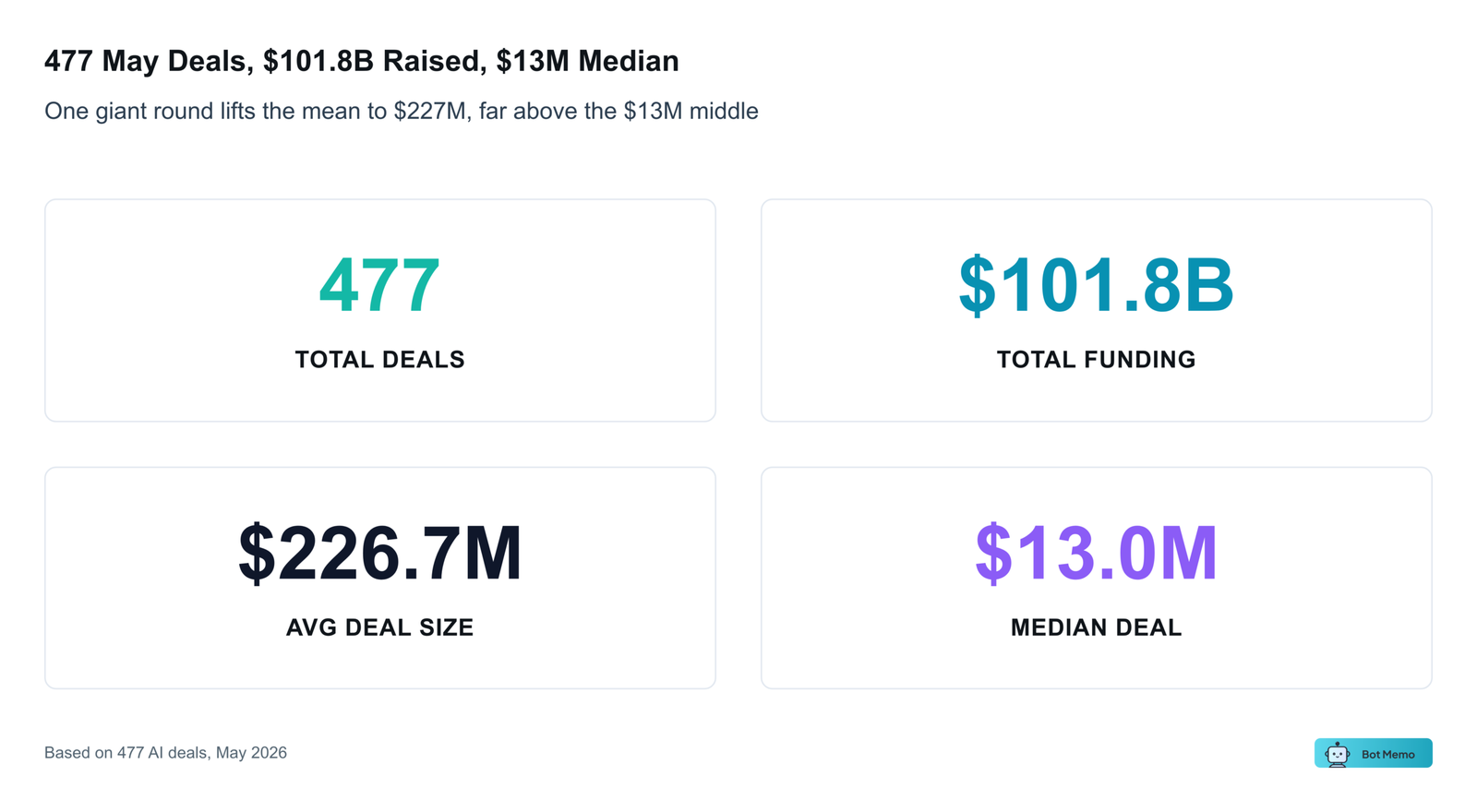

May 2026 logged 477 deals and $101.77B raised, but a single $65B Anthropic round bends every dollar chart. Weight by deal count and a three-hub, multi-market month appears.

On this page

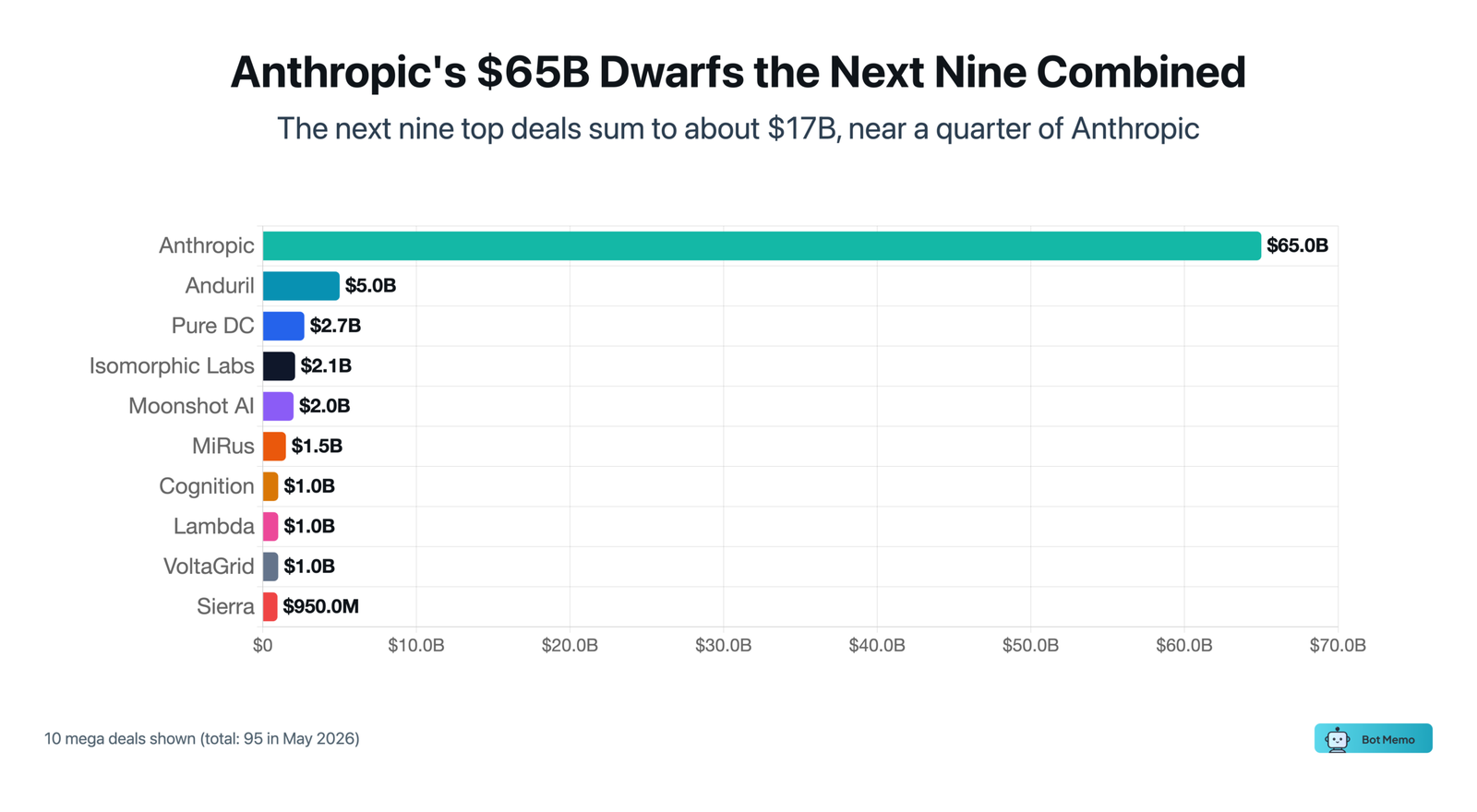

One round is doing all the talking

May 2026 looks like a blowout: 477 AI deals and $101.77B raised. But almost two thirds of those dollars sit inside a single check. Anthropic closed a $65B round in late May, and that one raise drags every dollar chart toward San Francisco and the frontier labs.

You can see the distortion in two numbers. The month posted a $226.67M average versus a $13M median. When the middle of the market is roughly seventeen times smaller than the average, the average has stopped describing the market. It’s describing one company.

So this issue weights May by deal count instead, and a different map appears. A three-hub race for where deals actually happen. Defense capital pooling in one corner of the country. Brand-name funds writing growth-size checks while seed shops hold the line. And a builder movement that dominates deal volume yet barely registers in the dollar totals.

If the dollars track one company, start with the metric that doesn’t: what got funded, and in what.

May 2026 at a glance: 477 AI deals, $101.77B raised, a $13M median.

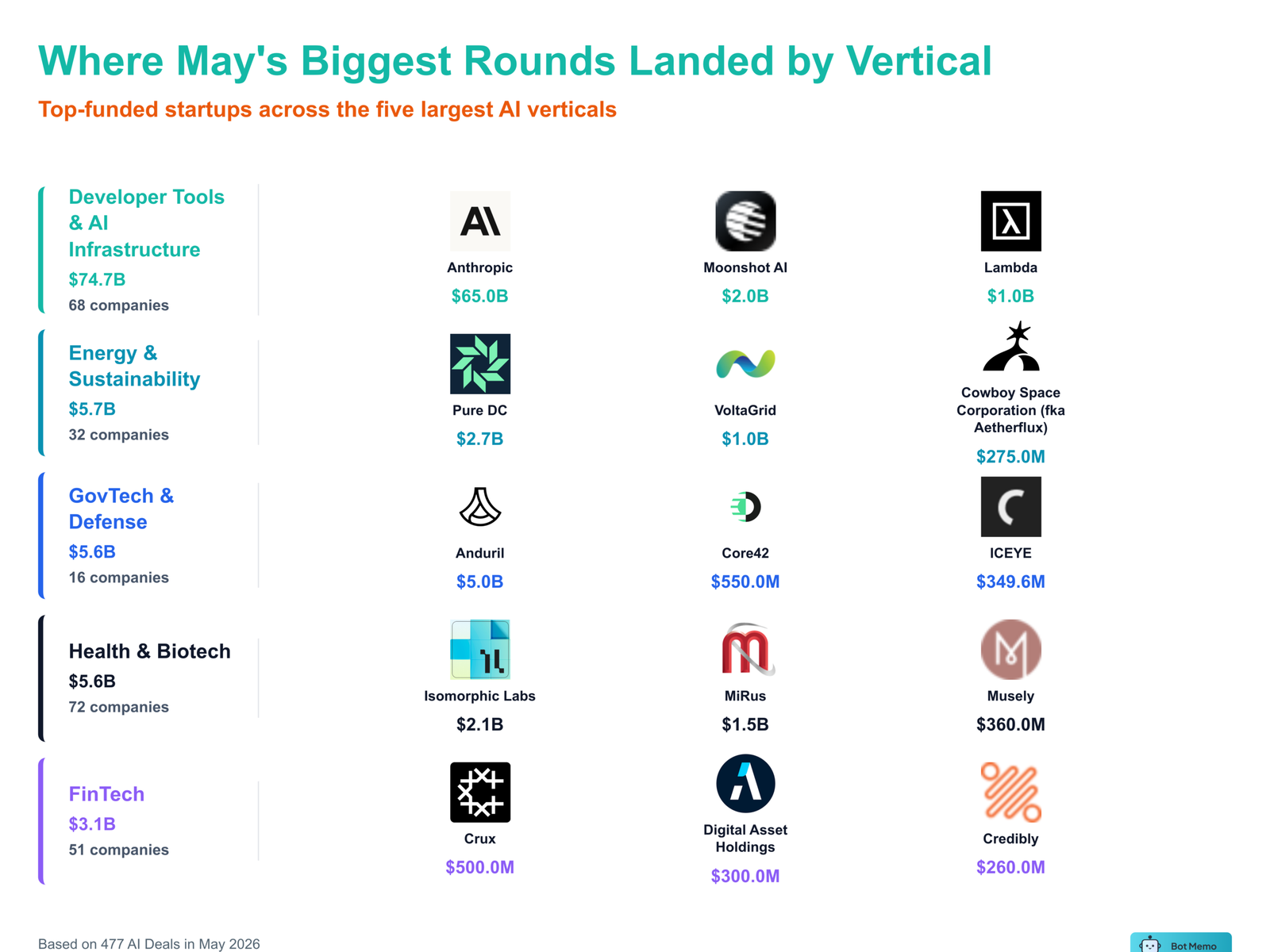

Where May’s AI capital landed.

The Builders Showed Up. The Capital Went Somewhere Else.

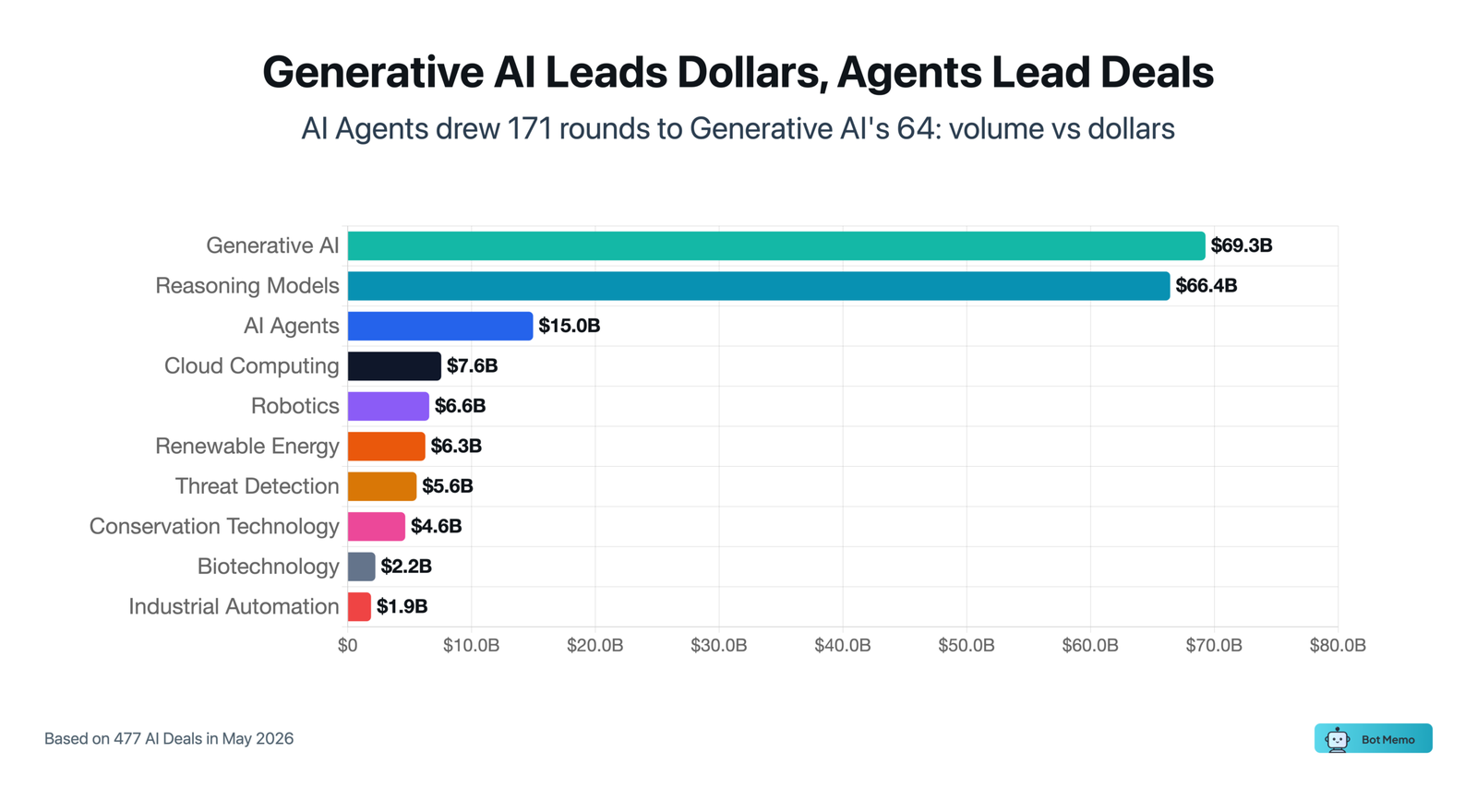

Count the deals and one tag towers over the rest. AI Agents booked 171 rounds in May, more than any other tag in the data. Count the dollars and that same category almost disappears. Those 171 agent deals pulled in just $14.97 billion, barely a fraction of what the labs raised.

Now look at where the money actually pooled. Generative AI ran only 64 deals yet absorbed $69.29 billion. Reasoning Models ran fewer still, 21 deals, and sat on $66.43 billion. Resist the urge to add those two figures together. The same giant rounds get tagged in both buckets, so stacking the totals double-counts the same handful of raises sitting underneath.

So the split is real. Agents win on volume. A thin set of generative and reasoning labs win on weight.

The volume side has names, and most of them sell tools rather than models. Vapi builds voice-agent infrastructure in San Francisco. CopilotKit ships open-source agent tooling out of Seattle. Judgment Labs sells evaluation rails that keep production agents honest. Modal runs the serverless GPU layer those agents deploy on. Each took a Series A through C check, real capital, none of it anywhere near lab scale.

One agent company broke the pattern. Cognition, the team behind an autonomous software engineer, crossed firmly into mega-round territory, the rare builder to land where the labs live.

The dollar side has its own outlier. Decart, a Tel Aviv lab training real-time generative video and world models, raised generative-scale capital well outside the US frontier shops.

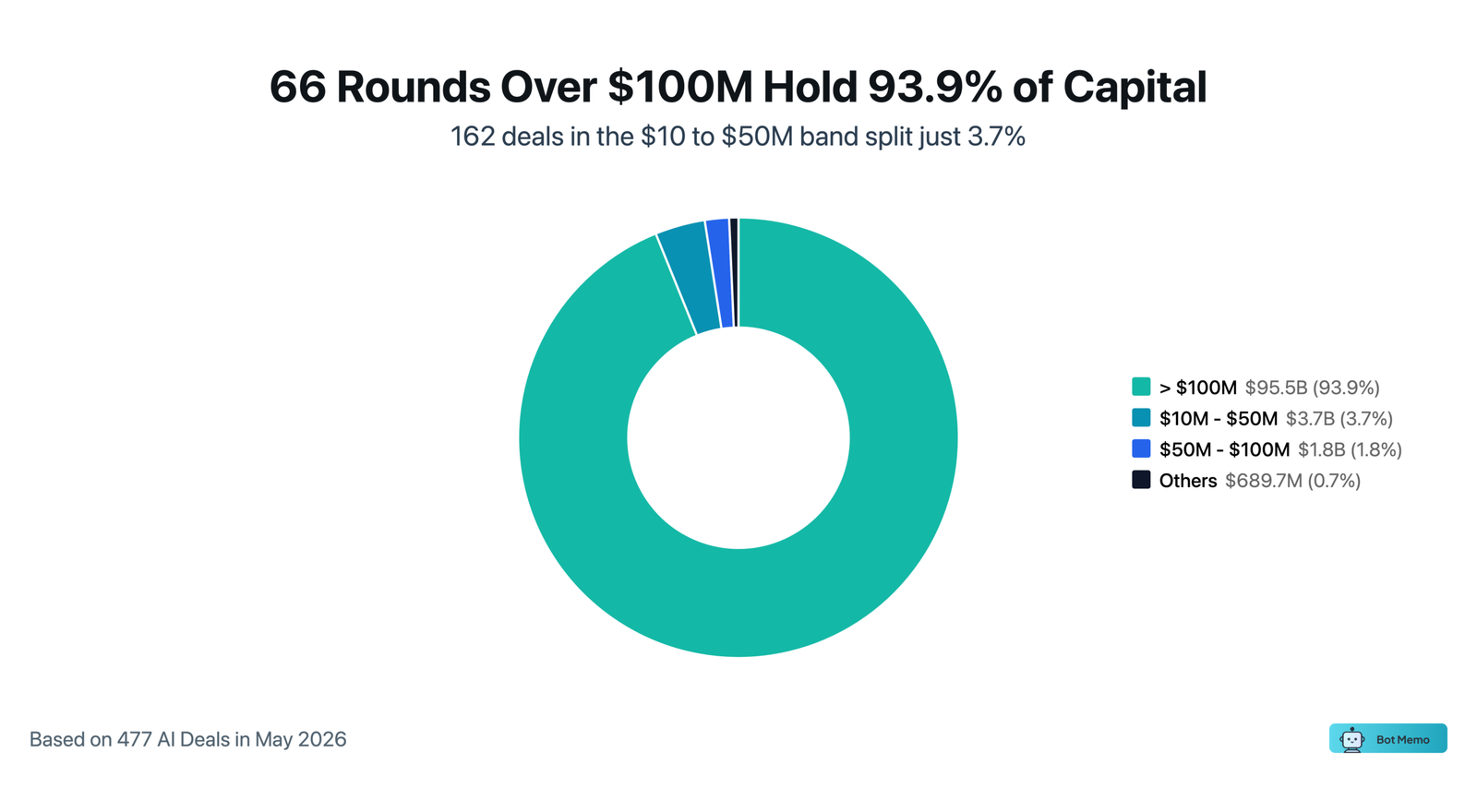

Step back and the concentration is stark. May logged 95 mega-deals, and they carried 95.6% of all funding, roughly $97.35 billion. The agent builders, counted in the hundreds, mostly sit outside that figure. Theme split is one fracture. Geography is the next, and defense is where it shows clearest.

AI Agents led by deal count; generative and reasoning labs led by dollars.

How May’s capital split across round sizes.

Defense Money Skipped San Francisco For Costa Mesa

As a sector, GovTech & Defense pulled $5,561.05M across 16 deals in May, the third-largest category by dollars in the month. Strip out one round and the sector nearly empties.

Anduril closed a $5B Series H, the second-biggest raise of the month, and it landed in Costa Mesa, not the Bay Area. That single deal carried close to the entire GovTech & Defense total on its own and pushed a one-deal metro into the top three by funding; the remaining fifteen deals split what little is left.

Brian Schimpf, the company’s co-founder, named the shift directly: “When we founded Anduril in 2017, defense was not a category that attracted significant venture investment. That has changed meaningfully over the last several years.”

The geography is the real tell. In Los Angeles, defense and govtech tied for the most common kind of AI deal last month, its largest local footprint anywhere, and not on the strength of one round. In San Francisco, the same category sat near the bottom of the table, a footnote against the city’s developer-tools and enterprise deals. The aerospace corridor and proximity to government pull defense AI south, away from San Francisco’s software gravity.

The category does not collapse into one city, though. Under the same banner, GovWell raised a Series A for civic software that automates permitting and compliance for local government, the opposite coast and the opposite hardware profile. The capital weight shows up abroad too. ICEYE, the Finnish operator of synthetic-aperture radar satellites, drew a $349.61M debt facility to fund its constellation, the kind of balance-sheet money that follows hardware rather than software.

Defense breaks the reflex that San Francisco routes everything. The broader deal map breaks it again.

May’s largest rounds by dollars. Defense is the lone such category near the top.

The Deal Map Is Wider Than the Dollar Map

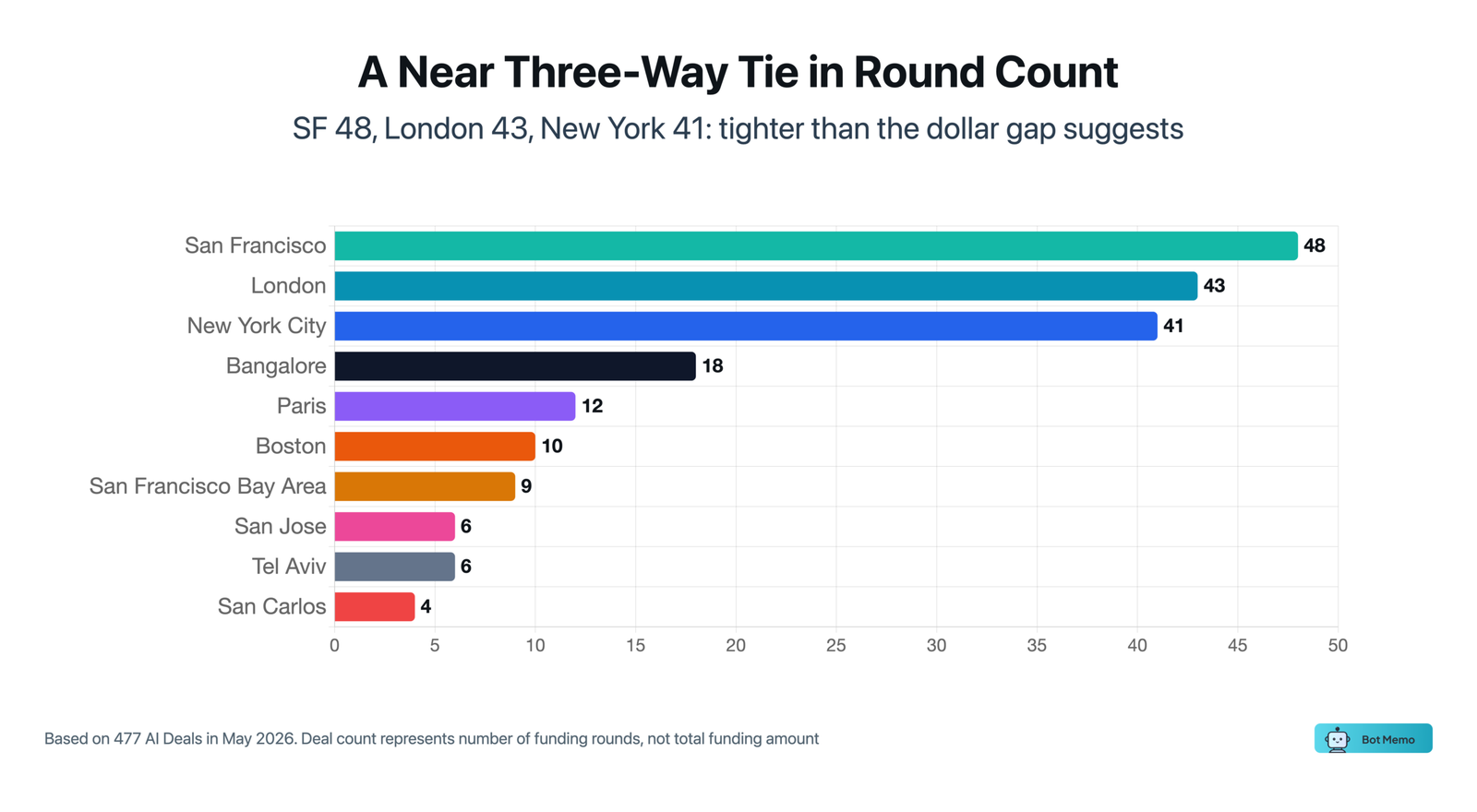

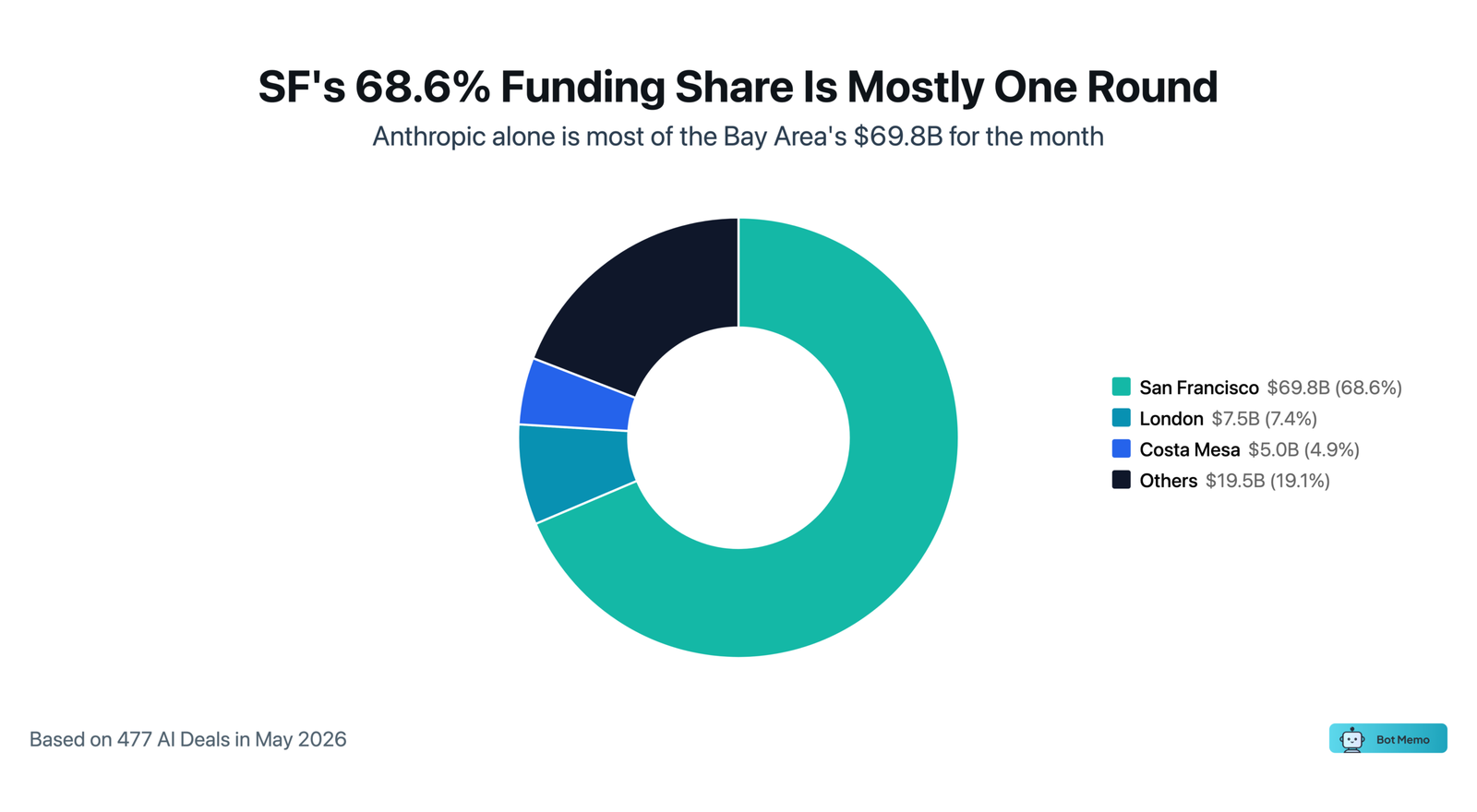

Rank May by dollars and San Francisco looks untouchable: San Francisco: 68.6% of the month’s AI funding in a single city. Rank the same month by deal count and that lead almost disappears.

By deal count, the three hubs nearly tie: 48 deals in San Francisco, 43 in London, 41 in New York. The dollar gap is one giant round wearing a city’s name, not a sign that the other two metros went quiet.

Strip the headline round out and San Francisco’s edge over London and New York is a rounding error. London logged 43 deals on 7.4% of the dollars. New York logged 41 deals on 3.1%. Those are working markets, not afterthoughts. By volume, the gap between the three hubs is a handful of deals, not a chasm.

Look at what filled those deal counts. London ran on applied, revenue-first companies. Adfin is the type, a London fintech putting AI agents to work moving money and collecting revenue for businesses. New York leaned into legal, compliance, and enterprise work rather than foundation-model labs. Zamp sits in exactly that lane, pointing AI agents at legal and compliance workflows.

The concentration was real, but it was narrow. The top five metros held 86.2% of May’s funding, yet the deals scattered across 176 separate locations. Same month, two very different shapes.

So the geography of money and the geography of deals are two different maps. The dollars stacked into one round in one city. The deals stayed broad.

If the map of deals is wider than the map of dollars, who was actually writing the checks, and how?

By deal count, San Francisco, London, and New York finish within seven deals.

Top five metros hold 86.2% of dollars while deals spread across 176 locations.

What the Checkbooks Say That the Headline Can’t

Sort May by who actually wrote the checks, and the brand-name funds split cleanly from the seed shops.

Andreessen Horowitz with 21 deals had 9 above $100M, and only a couple under ten million dollars, nearly $7.3B of capital attached to its name. Accel ran the same play at a tenth of the size: 10 deals, half of them at nine figures. Bain Capital Ventures with 5 deals had 4 above $100M, the most top-heavy of the group, $1.69B in all.

Now set that against Antler. Same seat at the top table, 8 deals, a combined $23.6M. Antler made zero deals above $100M, and most came in under five million dollars. That is the discipline the dollar headline never shows.

These tallies hand every fund in a syndicate credit for the whole round, so a name on a deal means a check landed there; it does not mean the fund led it.

You can watch both habits inside a single week. CodeIntegrity, a San Francisco startup building runtime guardrails for unpredictable AI agents, closed a $5M seed with Antler in the syndicate, the sub-ten-million check that defines a seed specialist’s book. Days earlier, a Bay Area robotics maker raised a nine-figure Series B, and its investor list read like a reunion of funds that built their names on seed and Series A bets: Andreessen Horowitz, Accel, and Bain Capital Ventures were all in.

Step back, and the lesson isn’t any single thread. It’s that May has no one winner, only a winner per ruler. Sort by dollars and one San Francisco round owns the month. Sort by deal count, by geography, or by check size and the crown keeps moving, to three hubs, to the Los Angeles aerospace corridor, to the seed shops that held their discipline. The headline picked the one ruler that flatters concentration.

Weighted by dollars, May belonged to one round. Weighted by where the checks actually landed, and at what size, it belonged to the market that round was sitting on top of.

Your take

Will June’s AI funding concentration loosen, or does one mega-round define every month now?

- It loosens. May was an Anthropic anomaly.

- It holds. The frontier labs keep eating the dollar share.

- It tightens further. The gap between the top round and everyone else keeps widening.

Methodology

Based on 477 AI funding deals tracked by Bot Memo between May 1 and May 31, 2026.

Source analysis SHA-256: 56e2cca33871af0e1e1a2f4f4e53119a466c7ffd3469ae31fdb967720132c20a

Data source: Public funding announcements, company announcements, regulatory filings, press releases, and direct founder submissions.

Scope: AI startup funding worldwide (176 unique locations).

AI Classification: AI Native: AI is foundational to the product. AI Augmented: existing product enhanced with AI. AI Adjacent: enables AI infrastructure. AI Platforms: builds foundation models or chips.

Multi-attribution: Companies operating across multiple verticals or cities are attributed to each. Investor totals reflect participation, not exclusive deployment.

Deal size bands: <$1M, $1-5M, $5-10M, $10-25M, $25-50M, $50-100M, $100M+.

Limitations: Funding amounts are based on public announcements and may not reflect total capital deployed.

About the author

Editorial Staff

The Editorial Staff at Bot Memo is a team of writers, analysts, and AI agents dedicated to mapping the global AI startup ecosystem. Led by Chintan Zalani, the team tracks thousands of funding rounds, classifies companies across verticals, and distills it all into actionable intelligence for investors and founders.